When Everyone Else Hesitates, Prepared Buyers Win

2026 has been a busy year for property. Rate rises, cost-of-living pressure, a federal budget that impacted confidence. The headlines make it easy to stay put. But underneath the noise, the conditions for first home buyers in Victoria are more helpful than most people realise. Here's what the data actually shows.

Property news in 2026 has given plenty of people a reason to pause. Three interest rate rises. Cost of living that won't sit still. A federal budget that unsettled the market. Property confidence is down and prices have softened.

That sounds like a reason to wait. But it's actually the perfect time to make your move—if you're ready.

With Melbourne's labour market resilient and investor competition easing, first home buyers are finding more room to move in Victoria's outer suburbs in 2026.

Unemployment remains low

Australia's unemployment rate is running at around 4.3 to 4.5 per cent, which is low by historical standards. For context, it hit over 11 per cent in 1992 and nearly 7 per cent during COVID. Victoria's unemployment rate is slightly higher at 4.7 per cent, but the labour market overall remains resilient, with total employment continuing to grow year-on-year.

What this means practically: if you have steady employment and a deposit, your borrowing position is probably stronger than the headlines suggest.

Rents are rising, and may rise further

The May 2026 Federal Budget announced the abolition of negative gearing for established residential properties purchased after 12 May 2026 for new investors, taking effect from 1 July 2027. Most analysts are warning this is likely to worsen the rental market further, because some investors who would have bought rental properties will hold off.

The stock that investors typically buy, entry-level homes and units in outer suburbs, is exactly the stock first home buyers are looking at. With investors less active in that space, buyers face less competition. At the same time, the incentive to keep renting rather than buy your own place is steadily eroding, because rents are going up and there's no guarantee that changes any time soon.

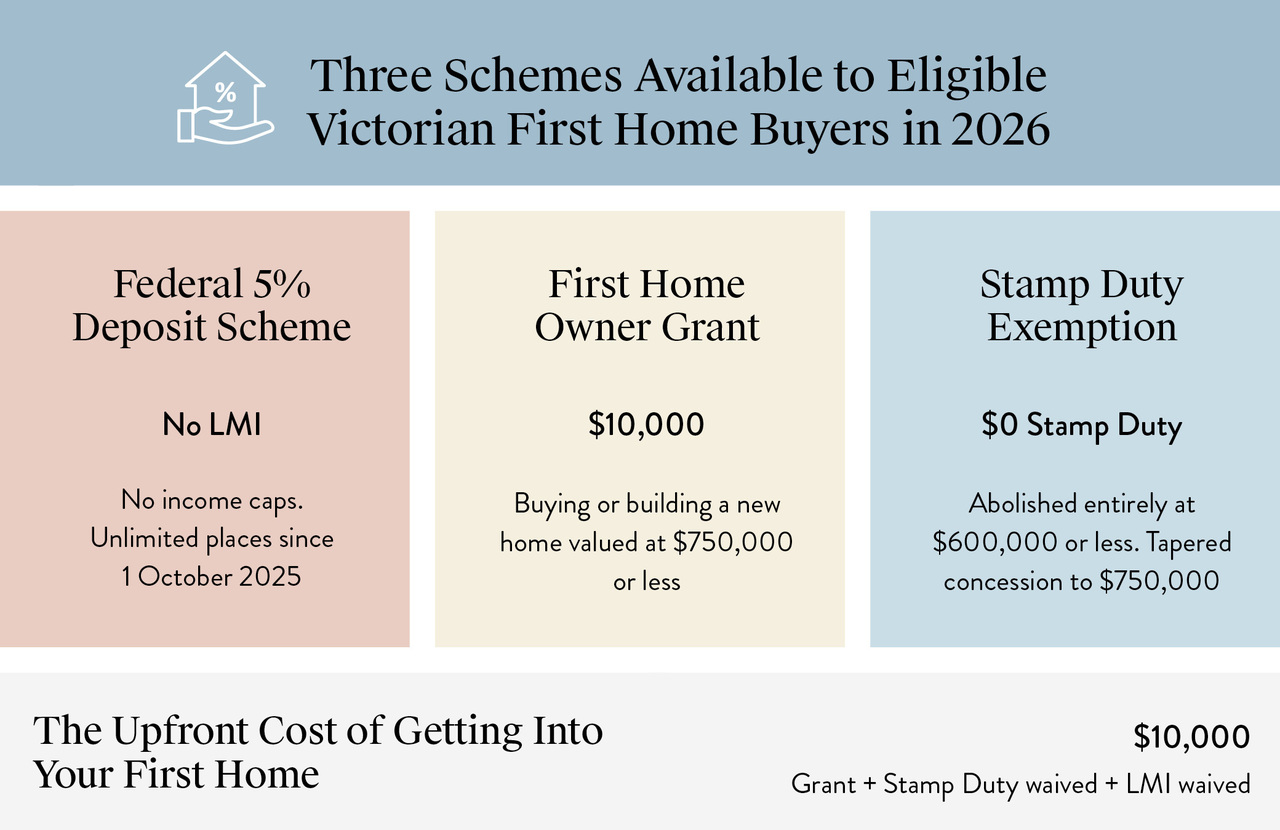

Eligible first home buyers in Victoria can stack the federal 5% Deposit Scheme, the $10,000 First Home Owner Grant and stamp duty exemptions to significantly reduce upfront costs.

The deposit hurdle is lower than ever

One of the most significant changes to shift in favour of first home buyers over the past year is the expansion of the federal government's 5% Deposit Scheme. Since 1 October 2025, the scheme has been expanded to offer unlimited places, higher property price caps, and no income caps, allowing eligible first home buyers to purchase with a deposit as low as 5% without paying Lenders Mortgage Insurance (LMI).

LMI on a high-LVR mortgage can add tens of thousands of dollars to the cost of your loan. Under the scheme, the government acts as guarantor for the gap between your deposit and the 20% threshold, so that cost is waived entirely. Since it started in 2020, the scheme has supported more than 248,000 Australians into home ownership, with its reach growing to support more than 1 in 3 first home buyers nationally.

Victoria has its own stack of support

On top of the federal scheme, the Victorian government provides a meaningful set of incentives for first home buyers that can make a genuine difference to your upfront position.

If you're buying or building a new home valued at $750,000 or less, you may be eligible for the $10,000 First Home Owner Grant. Stamp duty is abolished entirely for first home buyers purchasing at $600,000 or less, with a tapered concession for purchases up to $750,000.

Buying off-the-plan (ie: a home or apartment that’s not built yet) also attracts stamp duty concessions depending on the type of property and its value.

Stack the federal 5% Deposit Scheme, the First Home Owner Grant, and the stamp duty exemptions together, and the upfront cost of getting into your first home looks considerably different from what most people assume.

Carlisle's EasyLiving fixed-price homes come with premium inclusions as standard and a 20-week build guarantee, as seen in the Brooklyn 27 at Newhaven Estate, Tarneit.

It's a buyer's market right now

Melbourne dwelling values have eased over the last quarter. More listings and softer buyer demand mean buyers have more choice.

Melbourne's outer growth corridors continue to deliver land, with active estates across the north, west, and south-east. This means that for buyers considering a house and land package, there is genuine choice: competitive pricing, a range of locations, and the ability to lock in a price before construction starts.

This is particularly relevant in the current rate environment. When you build new, you're typically not paying your mortgage until construction is complete, which gives you time to continue saving while your home is underway.

Where Carlisle EasyLiving fits

For first home buyers who are ready to move, Carlisle's EasyLiving range makes it simple.

EasyLiving homes come with fixed-price contracts, premium inclusions as standard, and Carlisle's 20-week build-time guarantee on single-storey Hebel homes. You're not negotiating your way through an upgrade list; the kitchens, bathrooms, and flooring included in the base price are the kind of thing other builders charge extra for.

Plus, for buyers ready to commit before June 30 and finance arranged through Mortgage Domayne, you pay only $2,000 until the slab stage, with the remainder of your 5% deposit and base stage payment due at that point. Prices are locked until June 2027, which matters in a market where construction costs have been rising. You know exactly what you're paying before you sign.

Explore the current EasyLiving offer at carlislehomes.com.au/offers/EasyLiving.

This content is general in nature and is not financial advice. Carlisle Homes does not provide financial or lending advice. Please seek independent advice relevant to your circumstances.