Tips for Buying in 2026: What First Home Buyers Need to Know

For many first home buyers, a new year brings a moment of reset – and buying a home often sits high on that list. While expanded government support and lower deposit pathways are opening doors, lenders remain cautious, and financial readiness is still essential.

Wanting to buy is one thing, but getting there takes more than enthusiasm. It’s about preparation rather than speed – understanding borrowing conditions, tightening personal finances and choosing a home that supports long-term stability.

With lending insights from Mark Polatkesen, General Manager at Mortgage Domayne, here’s what first home buyers should be thinking about as they plan their move into the market.

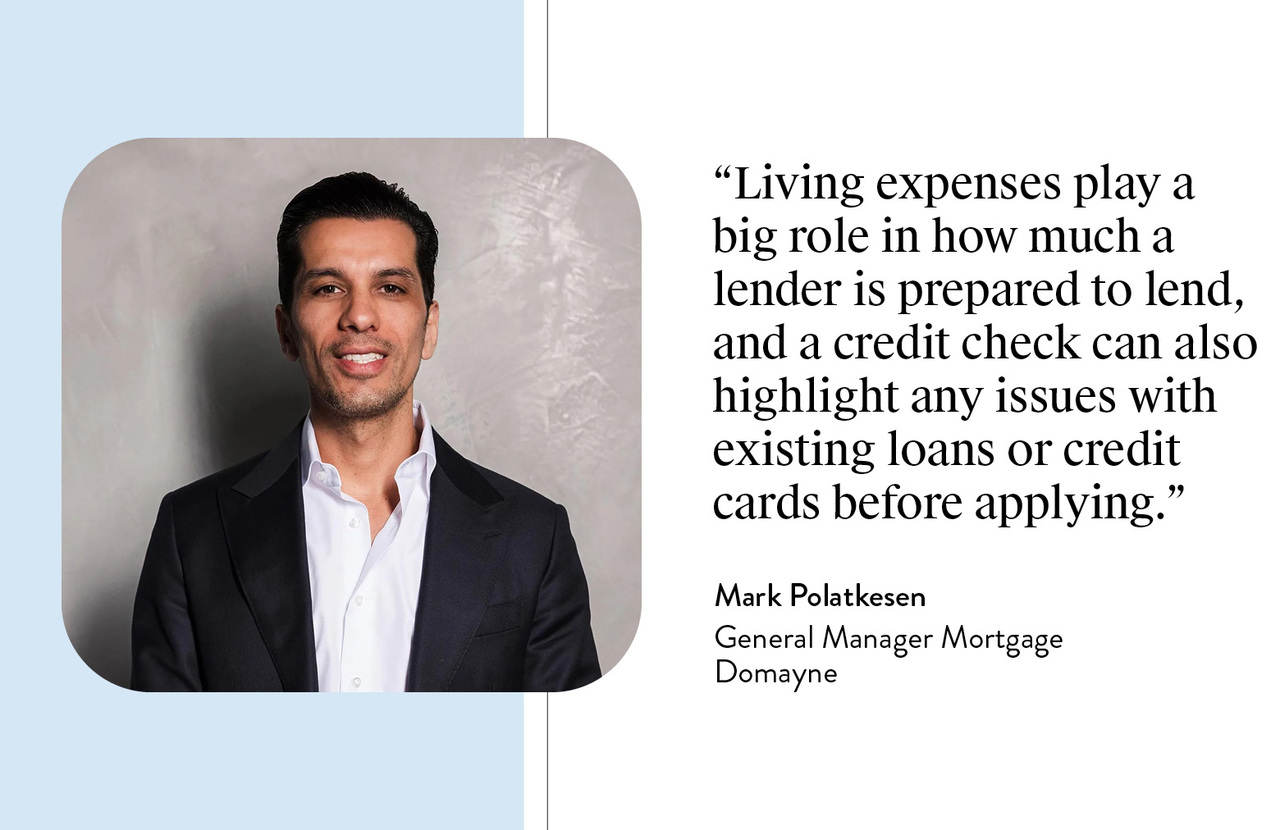

First home buyers can strengthen their home loan application by reviewing recent bank statements, reducing unnecessary expenses and understanding living costs, says Mark Polatkesen.

Resetting finances after the holiday season

The start of the year is the best time for first home buyers to reset their finances, particularly after the expense-heavy holiday period. Lenders don’t just assess your income, they closely examine spending behaviour, ongoing commitments and recent bank statements. A proactive financial tidy-up early in the year can make a noticeable difference when it comes time to seek loan approval.

“It’s always worth reviewing your last one to two months of bank statements and identifying recurring expenses like memberships or subscriptions you may no longer need,” says Mark. “Living expenses play a big role in how much a lender is prepared to lend, and a credit check can also highlight any issues with existing loans or credit cards before applying.”

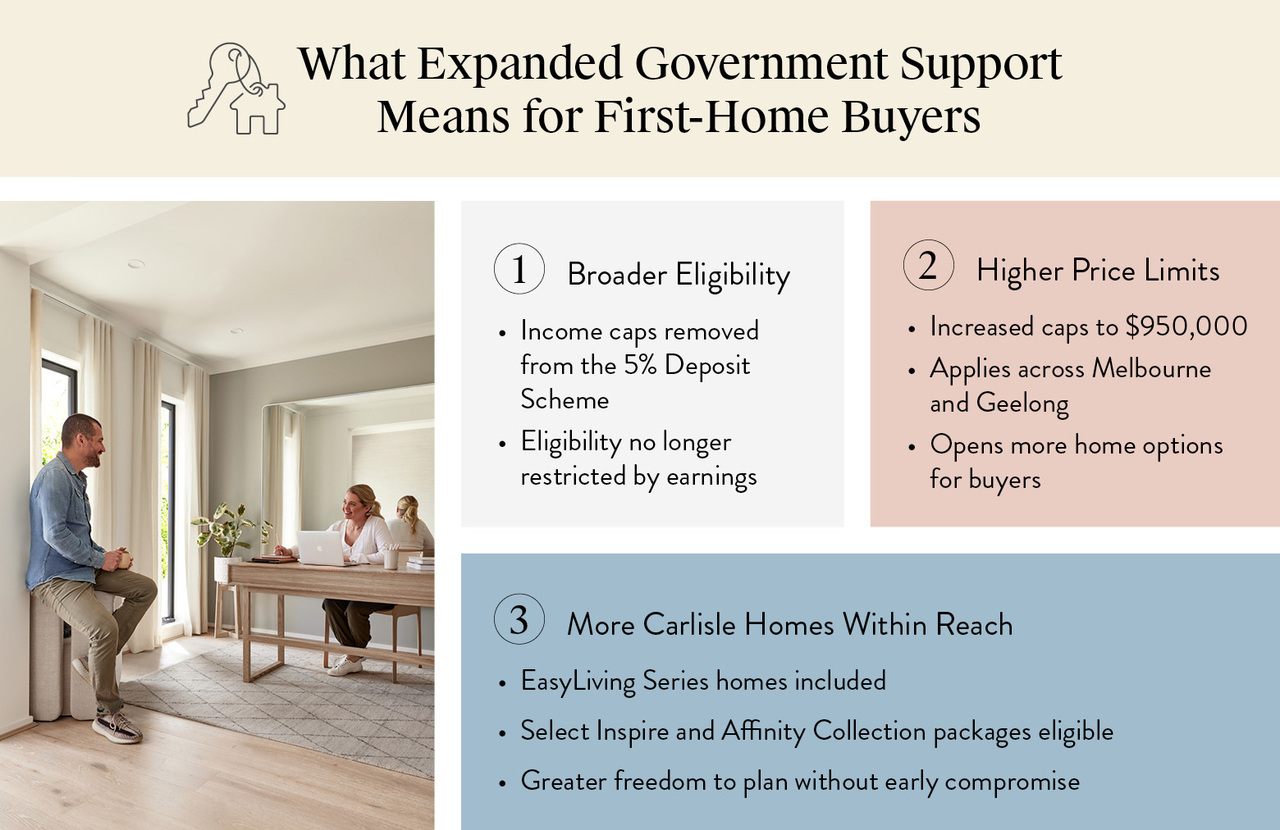

Expanded government support for first home buyers, including the Australian Government 5% Deposit Scheme, higher property price caps and broader eligibility, helping more Australians plan and buy with confidence.

Understanding expanded government support

Recent changes to government support have reshaped what’s possible for first-home buyers. Income caps attached to the Australian Government 5% Deposit Scheme (previously known as the First Home Buyer Guarantee) have been removed, meaning eligibility is no longer limited by buyers’ income.

Property price caps have also increased from $800,000 to $950,000 for Melbourne and Geelong, with many EasyLiving Series homes falling within this range, as do some Inspire and Affinity Collection packages. Combined, these changes give first-home buyers more room to plan rather than having to compromise prematurely.

“One thing many buyers don’t realise is that not all lenders participate in this scheme, so it’s important to work with a lender who can assist,” says Mark. “Permanent residents are also eligible if they’re first home buyers, and single parents with dependants may qualify with as little as a 2% deposit.”

Borrowing power, deposits and realistic expectations

Even with lower deposit options available, lenders continue to assess serviceability carefully, meaning your ability to make repayments. Borrowing power is influenced not only by income, but by existing debts, credit limits and day-to-day spending habits. Credit cards, in particular, can have a larger impact than many buyers realise, even when balances are cleared.

“Credit cards are a common issue,” Mark explains. “Even if there’s no balance owing, lenders assess the card based on its limit. The higher the limit, the less you can borrow. Reducing unnecessary debts and keeping living expenses in check can significantly improve borrowing capacity.”

Choosing a value-focused EasyLiving home helps first home buyers gain financial confidence through upfront pricing, clearer costs and reduced risk of budget surprises during the build process.

Why home choice matters for first home buyers

The type of home chosen plays a critical role in financial confidence. Value-focused options, such as Carlisle’s EasyLiving homes, are designed to remove uncertainty early by clearly defining costs upfront. For first home buyers, this clarity supports better decision-making and reduces the likelihood of financial surprises emerging mid-build, when changes can be costly and disruptive to loan approvals.

“The value-for-money approach of an EasyLiving home, combined with the generous standard inclusions, gives buyers much greater transparency around costs,” says Mark. “That’s especially important for those working within tighter borrowing limits, as it helps reduce the risk of budget blowouts. The fast contract process is another advantage, as it means pre-approvals are less likely to lapse mid-process.”

From New Year’s goal to new keys

For first home buyers, the path forward is clear – get informed, get organised and choose a home that meets your financial goals from day one. With clear costs, quality inclusions and a value-focused approach like Carlisle’s EasyLiving homes, building your first home can move from a new-year goal to a confident, well-planned next step.

Ready to turn your first-home plans into reality? Discover how the EasyLiving Series can help you get there sooner.