Should You Fix Your Home Loan in 2023?

Interest rates are on the rise, so we’re answering the question every homeowner is asking right now: should I fix my home loan in 2023?

Whether you’re a wannabe first-home buyer or a seasoned investor, you’re probably watching interest rates carefully. It’s no secret they have risen sharply in the last year, with the cash rate going from a record low of 0.1% to 3.1% as of December 2022. And there is a possibility that rates will rise again.

Typically, in order to make a profit, banks offer home loan interest rates that are around 2.5% higher than the cash rate. So in February 2023, the average variable rate for a $400,000 home loan (assuming owner-occupied and a 20% deposit or higher) was 5.69% per annum (up from 5.64% per annum last month).

With all of that in mind, is fixing your rate now a wise decision?

Fixing your home loan gives you more budget certainty and protects you from interest rate hikes, but there is less flexibility.

What are the differences between fixed and variable rate loans?

Let’s start with a quick refresher as to what we’re talking about.

A fixed rate loan allows you to ‘lock in’ an interest rate for a fixed term. The term can be any length, but the most common options in Australia are between one and five years. During that time, your monthly mortgage payment will be the same no matter whether interest rates fluctuate.

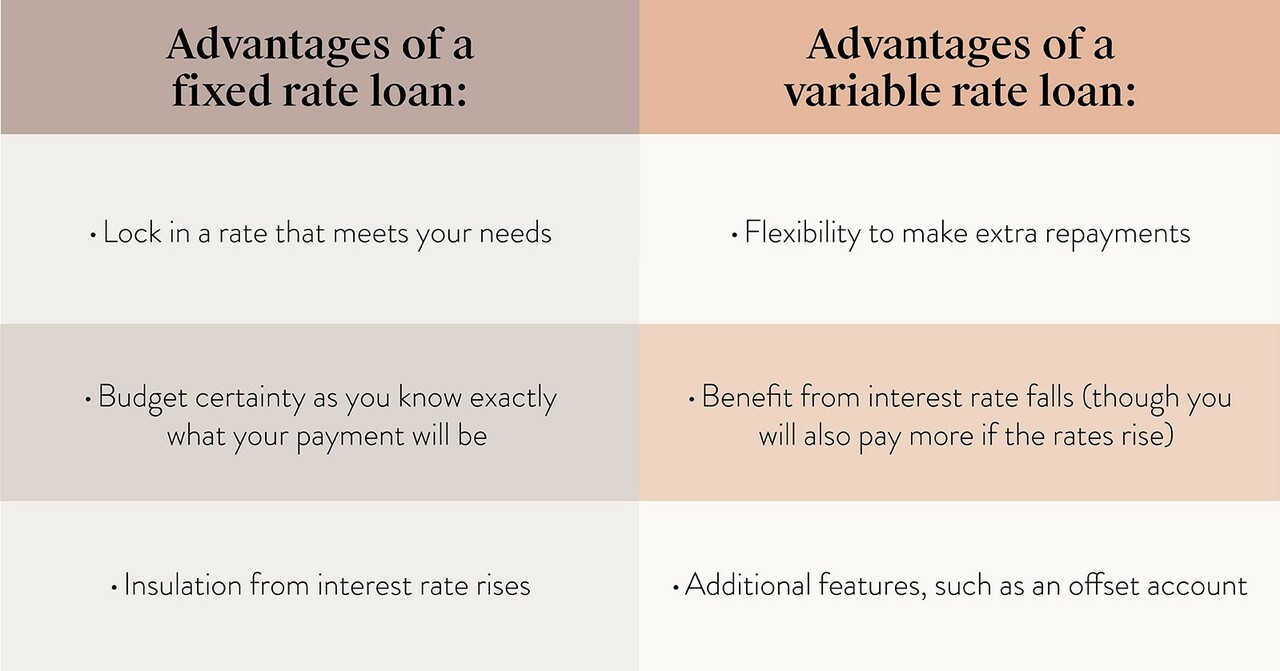

Advantages of a fixed rate loan include:

- Insulation from interest rate rises.

- Budget certainty as you know exactly what your payment will be.

Variable rate loans follow interest rates. Your mortgage repayment is made up of a principal repayment amount and an interest amount. If interest rates go up, the interest portion of your repayment also goes up. Of course, if rates go down, your repayment decreases.

Advantages of a variable rate loan include:

- Flexibility, as these loans allow you to make extra repayments, which fixed rate loans either limit or do not allow at all.

- Benefiting from interest rate falls, although you will also pay more if the rate rises.

- Additional features, such as an offset account, which are typically not available for fixed rate loans.

If you think interest rates will rise again, you’re better off fixing your rate now to lock it in at the lower rate.

How do I decide whether to fix my loan?

Essentially, deciding whether to fix your rate is about trying to predict the future. If you think interest rates will rise again, you’re better off fixing your rate now to lock it in at the lower rate. If you think they’ll fall, you may want to stay variable.

It’s worth noting that fixed rate loans tend to rise during periods of low interest rates. While prior to 2020, fixed rate loans only accounted for about 20% of all home loans, they rose to a record high of 46% in July 2021, coinciding with the record low cash rate. Deciding whether to fix your home loan depends on your financial goals and current market conditions. Use our Home Loan Comparison Calculator to weigh the pros and cons of fixed versus variable loan options.

Will interest rates keep rising?

The most likely answer is yes, at least in the short term.

The reason the Reserve Bank of Australia (RBA) has hiked interest rates so dramatically is to try and curb inflation. They have a target band of 2-3% inflation, and home loan interest rates are the main tool at their disposal to influence consumer spending. When interest rates go up, mortgage repayments go up with them and households cut back on unnecessary spending. In theory, this helps to reduces inflationary pressure.

While this is a simplistic analysis, the takeaway for homeowners is this: if inflation remains high, it is more likely that the RBA will continue raising interest rates. The latest Consumer Price Index figures for the December quarter show an annual inflation number of 7.8% (the highest since 1990 and well above the target band of 3%).

It's important to consider your individual household needs and choose what works for you. A variable loan offers less certainty, but it might give you the flexibility you need.

Which loan meets my needs?

Of course, interest rate rises are only part of the story – your individual household needs should also be taken into account. Remember, variable loan offers less certainty, but more flexibility.

You may be able to find a package with an offset account, for example. This allows you to reduce the interest payable by having your salary paid into a transaction account that ‘offsets’ the interest on your home loan.

A variable loan also allows you to make extra repayments. Just a few hundred dollars extra a month – or putting tax refunds and other ‘windfalls’ into your home loan – can slice years off your loan.

You are also more able to switch to a new lender if they’re offering more attractive rates or ‘cash back’ options on refinances. Fixed rate home loans come with ‘break fees’, which can cost you a lot if you want to end the deal faster.

Still unsure? To help you choose the right option, talk to one of our in-house construction finance specialists. And if you’re ready to buy, call Carlisle Homes on 1300 328 045 to discuss the perfect house and land package for you.