First Home Finance: What You Actually Need to Know Before You Start

Buying your first home is exciting, but the finance side can feel overwhelming. Mark Polatkesen, Managing Director at Mortgage Domayne, shares practical tips to help first home buyers understand their options, take advantage of government support, and feel confident taking the first step.

Buying your first home is one of the biggest financial decisions you will ever make, and it is completely normal to feel unsure about where to start. How much do you actually need for a deposit? What government support is out there? Should you talk to a bank or a broker? These are the questions that almost every first home buyer has, and the good news is that the answers are more encouraging than you might think.

We sat down with Mark Polatkesen, Managing Directorat Mortgage Domayne, to break down the key things first home buyers need to know in 2026.

First home buyer guidance from Mark Polatkesen at Mortgage Domayne, covering deposits, government support and practical steps towards home ownership.

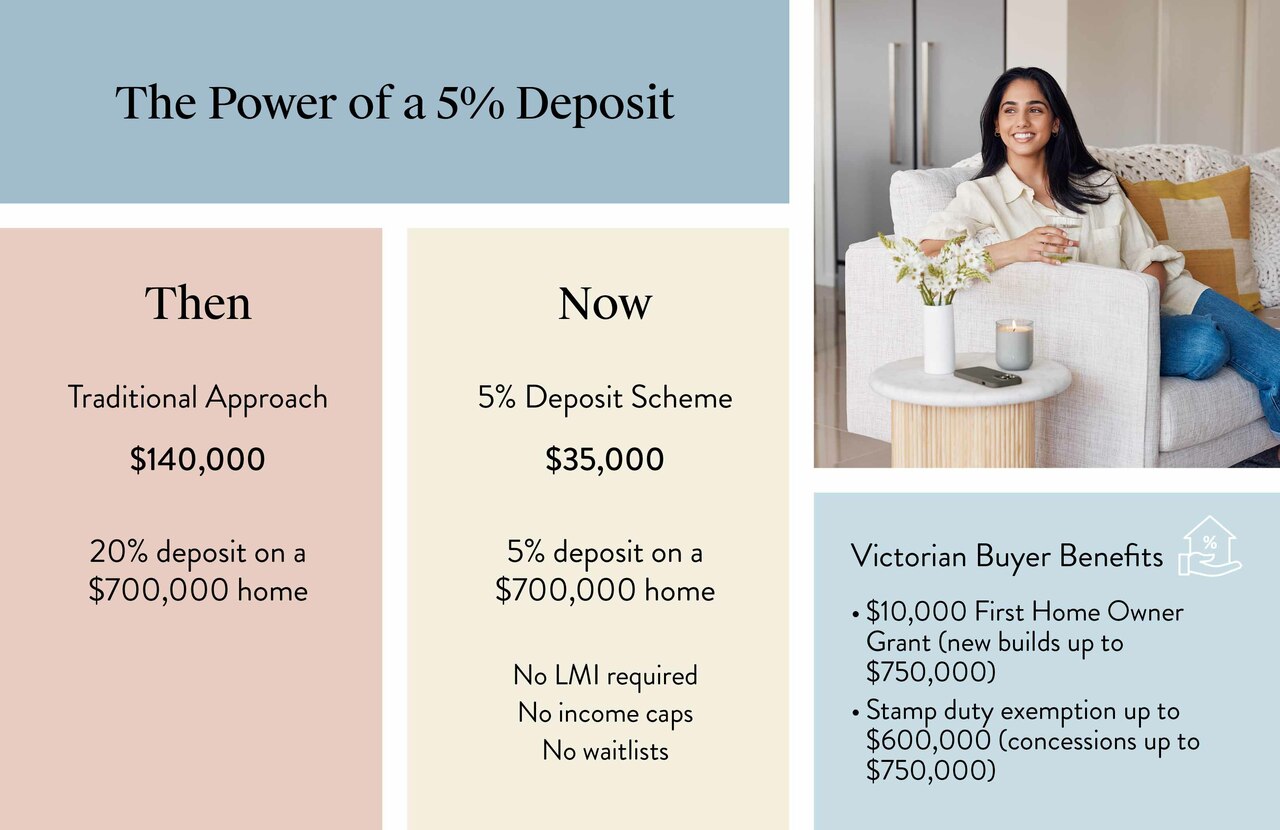

The deposit is not as big as you think

For a long time, the assumption was that you needed a 20% deposit to buy a home. That is no longer the case. The Australian Government’s 5% Deposit Scheme, expanded in October 2025, allows eligible first home buyers to purchase with just a 5% deposit, with the government guaranteeing the remaining portion up to 20%. The big change is that there are now no income caps, no waitlists, and no Lenders Mortgage Insurance (LMI) to pay.

“This has been a gamechanger for first home buyers,” says Mark. “For someone buying a $700,000 home, we are talking about a deposit of $35,000 instead of $140,000. That is a very different savings target, and it means a lot of people who thought homeownership was years away can realistically start planning now.”

The First Home Owner Grant of $10,000 applies to builds up to $750,000, but that figure is just the build contract and doesn't include the land value. And while the example above is based on a $700,000 home, the First Home Guarantee scheme allows eligible buyers to purchase up to $950,000 with only a 5% deposit.

First home buyers can enter the market sooner with a 5% deposit, supported by government schemes and expert guidance from Mortgage Domayne.

What about a parental guarantor?

If your parents own a home, a parental guarantee is another option worth exploring. It doesn't mean they hand over cash; instead, they offer a portion of their home equity as additional security on your loan, which can reduce your loan-to-value ratio and help you avoid LMI altogether.

“It is a really practical way for parents to help without dipping into their savings,” Mark explains. “The guarantee is typically limited to the portion above 80%, and once you have built enough equity through repayments or property growth, the guarantee can be released. Most of the time that happens within a few years.”

It is worth noting that being a guarantor does carry risk. If the borrower cannot make repayments, the guarantor is liable for the guaranteed amount. That is why it is important for both parties to get independent financial and legal advice before going ahead.

Set a realistic budget (and stick to it)

One of the most common mistakes Mark sees is buyers focusing only on the purchase price without factoring in the full cost of buying and building. There are legal fees, connection costs, landscaping, window furnishings, and the everyday costs of running a household to consider.

“My advice is to work backwards from what you can comfortably afford to repay each month, not from the maximum a lender will approve you for,” says Mark. “Just because you can borrow $700,000 does not mean you should. Leave yourself breathing room.”

This is where building with Carlisle Homes can really help. Carlisle’s fixed-price builds mean you know exactly what you are paying from the start, with no hidden costs or surprise variations. Their EasyLiving Series is designed specifically for first home buyers, offering quality homes with premium inclusions at a price point that does not ask you to compromise on the things that matter. And with house and land packages, you can combine your land and home into one straightforward purchase, making budgeting simpler and more predictable.

Set a realistic budget with Mortgage Domayne’s expert advice and Carlisle’s EasyLiving fixed-price homes, as seen in the Oakmere Grand 34 at Newhaven, Tarneit Display Centre Gallery.

Broker or bank? Understanding your options

A question Mark gets asked constantly is whether to go to a bank or a mortgage broker. His answer is straightforward: a broker works for you, not for one particular lender.

“A broker has access to a panel of lenders and can compare products across the market to find the right fit for your situation,” he says. “They can also help you navigate the different government schemes, because the interaction between federal and state incentives can be complex. A good broker will make sure you are not leaving money on the table.”

When it comes to choosing a loan, Mark recommends paying attention to features like offset accounts, which let you reduce the interest you pay by holding savings against your loan balance, and redraw facilities, which give you access to any extra repayments you have made. Both can save you thousands over the life of your loan, so it is worth understanding how they work before you commit.

Start planning early (earlier than you think)

Mark’s strongest piece of advice for first home buyers is to start the finance conversation well before you start looking at properties or display homes.

“Get pre-approved so you know your budget. Map out a timeline that includes saving, purchasing land, your build period, and your expected site start date. The more you plan up front, the fewer surprises you will have along the way.”

And perhaps most importantly, surround yourself with the right people. A good mortgage broker, a supportive builder, a conveyancer you trust. Buying your first home is a team effort and having people in your corner who genuinely want to help makes the whole process feel a lot less daunting.

Carlisle Homes works closely with Mortgage Domayne to support first home buyers through every stage of the journey. If you are ready to take the first step, explore Carlisle’s range of house and land packages or visit a display home to see what is possible.

Disclaimer: This content is general in nature and is not financial advice. Carlisle Homes does not provide financial or lending advice. Please seek independent advice relevant to your circumstances.