How an RBA Rate Cut Could Boost Your Borrowing Power in 2026

With interest rate cuts back in focus, 2026 may present new opportunities for Australians planning to buy their first home. Decisions made by the Reserve Bank of Australia continue to influence borrowing power, home loan repayments and overall affordability across the housing market.

Understanding how a rate cut works, and what it could mean for your borrowing capacity, can help you plan with greater confidence. At Carlisle Homes, we support buyers with clear information and guidance, helping make sense of lending conditions as they evolve.

What happens to interest rates and home loans when the RBA cuts rates?

When the Reserve Bank of Australia (RBA) cuts the cash rate, it is making a broader monetary policy decision aimed at supporting Australia’s economy. This typically occurs when inflation is easing, economic activity is slowing, or there is a need to encourage spending and investment. The cash rate is the interest rate banks pay when borrowing money overnight, and it forms the foundation of Australia’s lending system.

Because banks rely on this funding, changes to the cash rate often influence the interest rates they charge customers. When the cash rate falls, banks may reduce interest rates on home loans, particularly variable-rate loans. These changes are not automatic or uniform, but a lower cash rate environment generally places downward pressure on borrowing costs.

For home buyers in 2026, this relationship matters because interest rate movements can affect both monthly repayments and how lenders assess affordability. Lower interest rates can reduce repayment amounts and interest costs over time, which may improve lending conditions and support borrowing power, depending on personal income, credit history and lender policy.

How does a rate cut increase your borrowing power?

A rate cut can increase borrowing power because lenders assess how much you can borrow based on your ability to meet loan repayments, both now and in the future. When interest rates are lower, the estimated repayments on a loan decrease, which can improve how affordable that loan appears under a lender’s assessment.

Banks calculate borrowing capacity using serviceability models that factor in income, expenses, existing debts and an interest rate buffer. This buffer is designed to ensure borrowers could still afford repayments if rates rise in the future. When base interest rates fall, the overall repayment calculation may reduce, even after buffers are applied.

In 2026, a lower interest rate environment may allow some buyers to qualify for a higher loan amount without increasing financial strain. While the impact varies depending on personal circumstances and lender policy, even a modest rate cut can influence borrowing capacity when combined with stable income and manageable living costs.

What opportunities could the 2025 rate cut create for home buyers in 2026?

A rate cut implemented in 2025 may have opened up several opportunities for home buyers, particularly those entering the market or planning their next move. While outcomes vary, lower interest rates can influence both affordability and buyer confidence in meaningful ways.

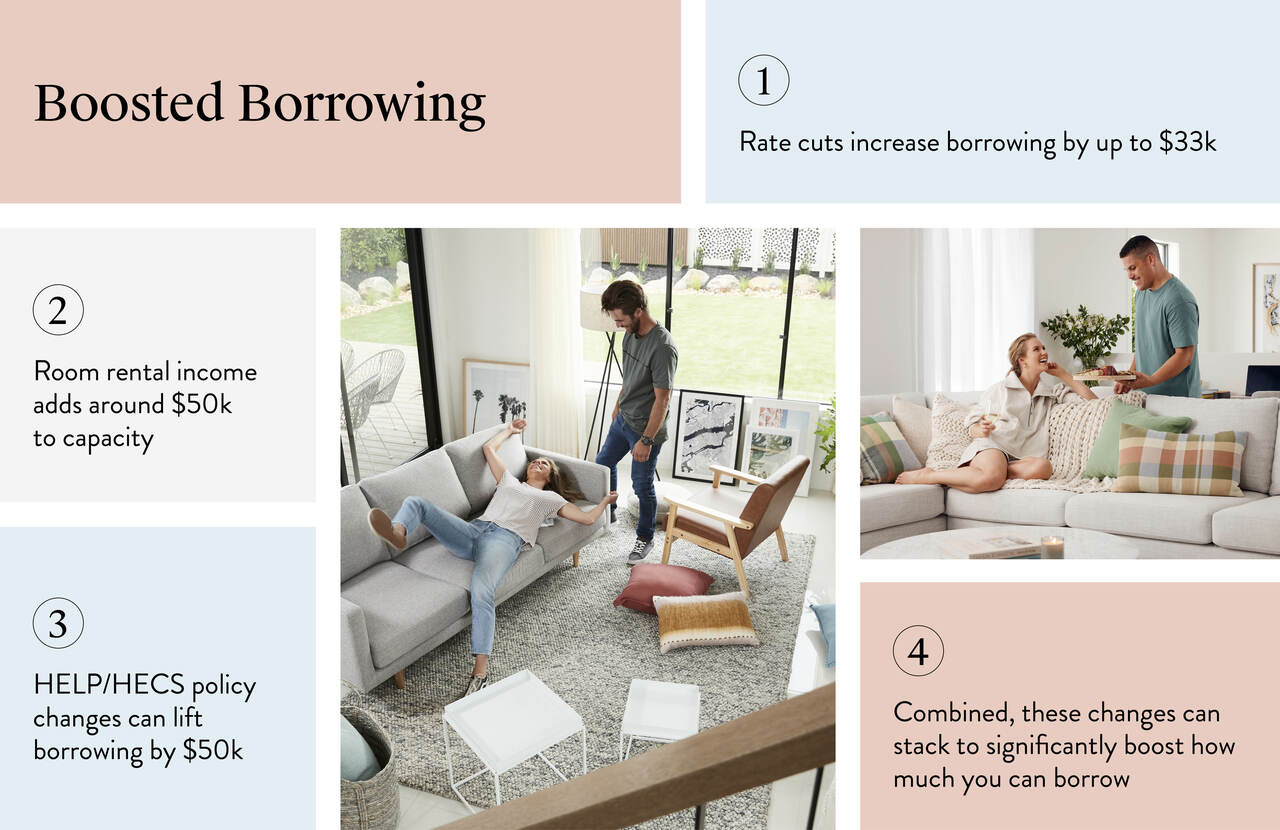

1. Improved borrowing power

Lower interest rates can reduce assessed loan repayments, which may allow some buyers to qualify for a higher loan amount without increasing financial strain. Recent changes aim to make it easier for first home buyers to enter the market. For example, Commonwealth Bank may offer an allowance of $150 per week for those renting out or boarding a room, potentially increasing borrowing power by around $50,000.

Updated HELP/HECS debt policies could also lessen the impact of student loans on borrowing capacity, adding another $50,000 to what you can borrow. What does that mean in practice? More options, better choices, and a greater chance to secure a home that truly fits your lifestyle and aspirations.

2. Lower monthly repayments

For buyers with variable-rate home loans, a rate cut may have reduced ongoing repayment costs, improving household cash flow and affordability. This extra cash could free up your finances, whether it’s for home improvements, savings, or just peace of mind.

3. Greater choice within budget

With improved borrowing capacity, some buyers may find they have access to a wider range of homes, locations or design options than previously possible. By lowering the deposit requirement to just 5% and removing the need for Lenders Mortgage Insurance, this reduces barriers and help more Australians enter the property market sooner.

4. Earlier entry into the market

Reduced borrowing costs can help some first home buyers move forward sooner, rather than delaying plans while saving a larger deposit. The Australian government has proposed a new 5% Deposit Scheme that could significantly expand the First Home Guarantee program. If implemented, it would remove existing income limits and place caps, making the scheme accessible to all eligible first-home buyers.

5. Increased market confidence

A rate cut often signals supportive economic conditions, which can lift buyer sentiment and encourage more Australians to consider home ownership.

How can you prepare now to make the most of a future rate cut?

While interest rate movements are outside an individual buyer’s control, there are practical steps you can take to be better prepared if another rate cut occurs. Planning ahead can help you respond with confidence and clarity when lending conditions shift.

Step 1: Review your financial position

Start by assessing your income, expenses, existing debts and savings. Lenders look closely at these factors when determining borrowing power, so understanding your current position helps identify areas that may need improvement.

Step 2: Strengthen your savings and repayment history

Building consistent savings and maintaining a strong repayment record can improve how lenders assess your application. Even small improvements in cash flow or savings habits can make a difference under serviceability checks.

Step 3: Reduce existing debt where possible

Paying down personal loans, credit cards or other liabilities can reduce financial strain and improve borrowing capacity. Lower debt levels can position you more favourably if interest rates fall and borrowing conditions ease.

Step 4: Explore finance pre-approval

Seeking finance pre-approval can help you understand how much you may be able to borrow under current conditions. If rates change in the future, having a clear baseline allows you to reassess quickly and act with confidence.

Ready to boost your borrowing power in 2026?

Changes to interest rates can create meaningful opportunities for home buyers, but preparation remains key. By understanding how rate cuts affect borrowing power and taking steps early, you can approach the home buying journey with greater confidence and clarity.

If you are considering your options in 2026, speaking with our consultants can help you understand how current lending conditions may apply to your personal circumstances. Our team is here to support you with clear guidance, from finance considerations through to planning your new home.