Why Now is a Good Time to Buy a House

Tired of renting? Find out the pros of buying a house in today’s market and how it could save you money and broaden your future buying potential.

With rents spiking across the country, Australians are once again asking themselves: is this a good time to buy a house? Buying or building a new home requires an initial outlay of money. If you can come up with a deposit, though, it can mean serious savings down the track as well as many home owner benefits.

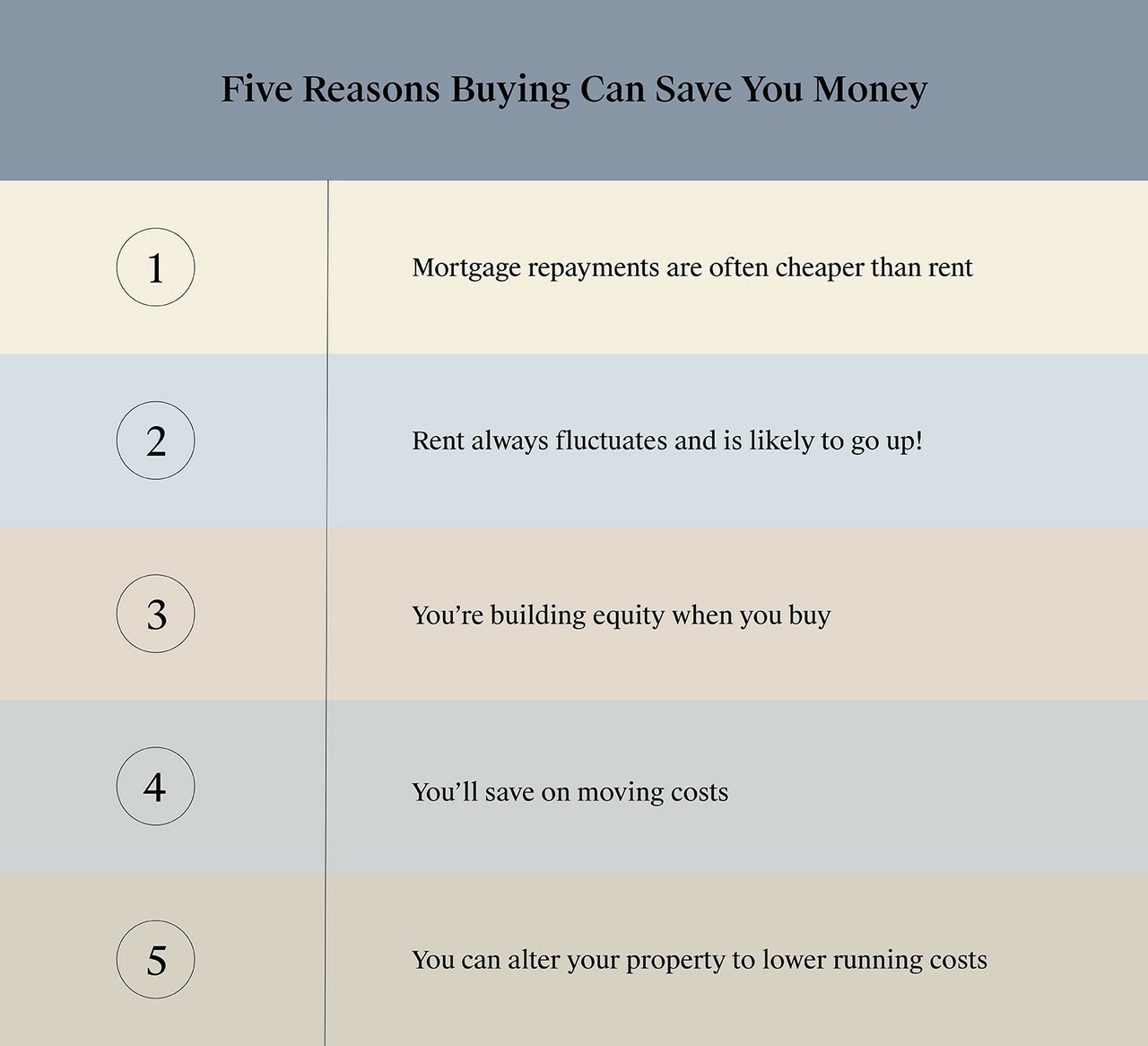

Here are five reasons why buying an established or new home can save you money.

There are many hidden costs to renting! Here we break down the five reasons why this is a good time to buy a house and how it might be more cost-effective in the long run.

1. Mortgage repayments are often cheaper than rent

Analysis from realestate.com.au indicates that buying is cheaper than renting for 56.8% of all Australian dwellings. This won’t come as news to anyone paying more in rent per week than their mortgage repayments would be for a similar home. The analysis also takes into account ‘hidden costs’ such as rates, taxes and maintenance, which are shouldered by a landlord in a tenancy arrangement.

It is more likely to be cheaper to buy a house in regional areas and the outer suburbs of capital cities. Renting is cheaper in the inner cities, especially in Sydney and Melbourne - although it’s worth noting that this analysis was undertaken a year ago, when both cities were still in and out of lockdown and many city apartments stood empty. Demand, and rental price, have soared in the subsequent months.

In Victoria, the five cheapest suburbs in which to buy (relative to renting) are:

- Waterford Park

- Rockbank

- Mickleham

- Milgrove

- Wollert

Going nowhere but up – rental hikes may steer you to choose a flexible home-loan plan, allowing you to save on mortgage payments down the track. Featured here: Scarborough Grand, Smiths Lane, Clyde North.

2. Rent always goes up

In the first year of your home-owning journey, mortgage repayments will cost on average 26% of your salary.

However, once you’ve locked that loan in place, there are limits to how much more the repayments could be. If you have a variable rate loan, interest rate rises might increase your minimum repayment, but only by a limited amount. For example, a 1% interest rate rise on a mortgage of $650,000 would be around $400 per month, or $100 per week. Any extra repayments you make on the principal of your loan will reduce that amount further.

But the pros of buying a house: wage growth and natural inflation means that, as a percentage of your income, your mortgage payment will go down. 20 years later, the average mortgage payment is only 15% of income. Renters, on the other hand, will have borne rent rises in line with inflation. In fact, in 2021/2, thanks to a tight rental market, capital city rental prices soared by 14.7% in a single year.

Understand your current rental expenses and housing budget with our Rent Affordability Calculator.

This is a good time to buy a house as it gives first-home buyers the opportunity to grow equity, which can increase purchasing power in the future.

3. Home owner benefits: You’re building equity!

How can equity save you money? There are a few ways.

Firstly, if you’re one of the large cohort of first-time buyers who buy with a deposit of less than 20%, you may have taken out lenders mortgage insurance as part of the deal. But you don’t have to wait until you’ve paid back a substantial amount of your loan to drop the extra cost. As your home increases in value, your loan decreases as a percentage of that value. For example, if you’ve bought a house and land package for $800,000 with a deposit of $80,000 and a loan of $720,000, your loan-to-value (LTV) ratio is 90%. Over time property values generally increase so your loan-to-value decreases. With many lenders when the ratio is 80% or under, you can drop the lenders mortgage insurance and save yourself thousands of dollars.

Secondly, a healthy amount of equity gives you options. If you’re a first home buyer purchasing with a minimum deposit, you might not have access to the full range of home loan products. Once you’ve built more equity, you’re an attractive proposition. Get back in touch with your mortgage broker and see whether it’s worth switching lenders for a better rate. Build your equity quicker with industry leading build times when you build with Carlisle’s EasyLiving Series.

4. You’ll save on moving costs

Renting in Australia can mean an insecure housing situation. Australia Post data suggests that renters move on average once every four years, often within the same suburb. However, that data is already lagging behind the post-pandemic reality for tenants. Rental stock has contracted sharply, and what is available is often being converted into short-stay accommodation. This means that some tenants are moving yearly, or even more often.

Moving house always incurs costs. There’s the cost of the removalists. Storage fees if there’s a gap between properties. Utility connection fees, mail redirection and very often, the cost of a professional cleaner to come in at the end of your lease. The more often you have to move, the more those fees rack up. Why buy a house? So you never have to move if you don't want to.

The benefit of being a home owner means you can implement cost-cutting additions and energy-efficient upgrades that are endless in possibility, an option that is often restricted to renters.

5. You can alter your property to lower running costs

Owning a home does come with maintenance costs. However, it also comes with a level of freedom to manipulate those costs. For example, you can install solar panels on your roof to cut down your electricity bills in the long term. Double glazed windows cut winter drafts and keep your home at an even temperature all year round. Even something as simple as a good quality carpet can make a significant difference. Learn more about the flooring decision here.

As a tenant, you may not be able to make any of these changes. You may also have limited scope to upgrade heating and cooling options to more efficient alternatives. This can make your utility bills higher than those of a homeowner.

Learn more about ways to save on energy bills here.

The media is reporting declining values across the housing market, which makes it a good time to buy a house.

The median house price in Melbourne's leafy inner suburbs has fallen annually by 4.5%. This is described as a market correction as the price growth for inner city housing has been unsustainable over the last few years and the market simply could not keep up with the pace. As the market resets and adjusts, it will settle at a more sustainable growth rate, and this is good news for home buyers in the long-term.

Also, the demand for outer suburbs and undeveloped land remains robust. The more affordable outer suburbs and land markets are showing more resilience than the established inner suburbs, which means the pro of buying your house now is that it will continue to grow in value in years to come.

With this market rebalance, and strong demand for undeveloped land, now is a good time to buy a house. And there are so many benefits to being a home owner that could save you money now and into the future.

Timing your home purchase is important, but understanding the full costs is just as crucial. Use our House Buying Cost Calculator to account for all expenses, including upfront costs, fees, and stamp duty.

Wondering if your finances put you in a position to buy? Chat to one of our in-house construction finance specialists. To find out more about buying the house and land package that suits your budget, call Carlisle Homes on 1300 328 045.