How to Future-Proof Your Finances

To get ahead, you must think beyond a paycheque-to-paycheque budget and start to make longer-term plans.

What does that mean? It means keeping an eye on the economic forecast, thinking about your career long-term and spotting opportunities where they arise. Above all, it means being prepared to change strategies when needed.

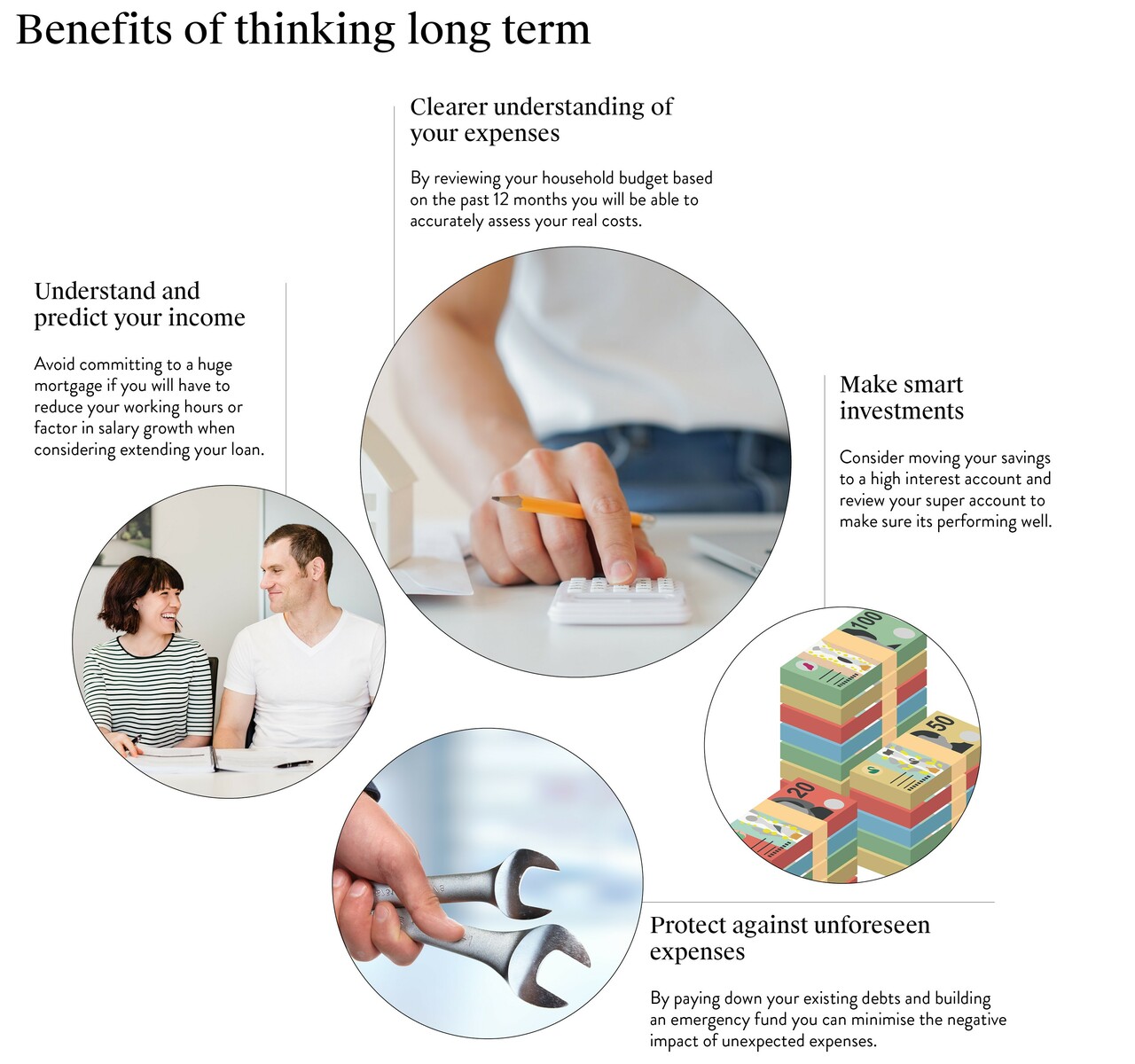

Thinking long-term has a range of benefits. For example:

Expenses

A very common mistake made by first-time budgeters is to look only at weekly or monthly costs. When those large annual costs, like a car service or Christmas, come along, you can be taken aback. A decent baseline for a household budget should look at the past 12 months of expenses to accurately assess your actual costs.

However, budgeting for the future takes this a step further. When you’re working out how much to send to savings, consider the following:

- Are any of your appliances ageing, and when will they need to be replaced? If you’re a homeowner, extend this to fittings such as the hot water system or air conditioning unit.

- Are you planning children, and what impact will that have on the family finances? If you have children, have you considered their changing costs? Expenses often drop when a child is old enough to go to school, and you’re relieved of the daycare bill. They may go up again when the children grow older and their requirements get more expensive.

Establishing a household budget is essential for managing your finances effectively. Utilising tools like our Household Budget Calculator can assist in organising your expenses and setting realistic savings goals.

Future-proofing your finances relies on you thinking long-term and spotting opportunities where they arise and being prepared to change strategies when needed.

Income

Spending your income responsibly is a good start. Looking ahead is better.

- What are your salary expectations over the next few years? There is no right answer to this question. You may be a new grad with a steep curve ahead of you or have reached the top of your current salary range. Perhaps you work part-time for family reasons, or you’re looking to wind back from a high-pressure

- Does that salary expectation match your spending plans? You don’t want to commit to a huge mortgage if you may have to reduce your working hours soon. Conversely, you might choose to extend yourself now to get the place of your dreams because you’re confident that your earning capacity will go up. Looking ahead is crucial to making smart decisions now.

Investing

Don’t worry; we’re not going to tell you to start studying the ASX 200 or going all-in on NFTs. Investing can be as simple as making sure your money is working for you. For example:

- Are your savings in a high-interest account? In recent years, the cash rate has been so low that savings accounts returned close to zero. Now, that landscape has changed. If you haven’t done so already, it’s worth looking around for a HISA that suits your goals.

- Are you comfortable with your superannuation fund? Performance and fees change between funds, so it’s worth taking an interest. Unless your employment ties you to a fund, switching is quick and easy.

Future-proofing your financial position can be a significant factor in you achieving your goals quicker.

Protecting

None of us can predict the future. But sensible financial planning allows for the hard times as well as the good. There are several things you can do now to protect your family and soften the blow if you lose your job or costs keep rising. Try:

- Paying down debt. When things are going well, it’s easy to be relaxed about taking on some debt. Whether it’s a car loan for that new vehicle you’ve had your eye on or a personal loan to splurge on a holiday, you’ll pay it back soon enough, right? However, being over-leveraged has its risks. In a downturn, debts can leave you very exposed. This is especially true for debts against a declining asset (one that loses value over time, like a car or mobile phone), as you may not recover the money if you sell. Consider paying off any consumer debt as fast as possible to reduce your overheads. At worst, you’ll be better able to cope with a cut in income. At best, you’ll be able to use that extra money to save for your goals.

- Building an emergency fund. This is the second must-do once you’re on top of any debts. An emergency fund. This is money that you can easily access (i.e., money held in a savings account rather than tied up in investments) in case you lose your job, are hit by sickness, or need to replace a big-ticket item in a hurry. Experts recommend that you shoot for an emergency fund of six months’ worth of expenses. If that sounds too daunting, remember, anything is better than nothing.

We may not be able to offer a crystal ball, but by looking long-term you'll be better prepared for whatever comes next.